|

|

The Retirement Savings Contributions Credit, aka the Saver’s Credit, is a lesser known tax credit that the IRS makes available to low and moderate income taxpayers who make retirement contributions to an IRA, 401K, 403B, 457, or any other IRS recognized retirement account.

|

|

As statistics show, only one in three eligible taxpayers are aware of this tax benefit.

|

|

|

|

The Saver’s Credit is an actual tax credit, not merely a tax deduction. While a tax deduction simply subtracts the value from your taxable income and you pay taxes on the remaining taxable income, a tax credit, on the other hand, actually gives you the entire dollar value back or subtracts the value from the taxes you owe, making it far more valuable monetarily than a deduction. In the case of the Saver’s Credit, it is non-refundable, meaning it can only be subtracted from the taxes you owe.

|

|

|

- The Saver's Credit was initially made available for tax years 2002 to 2006 under the Economic Growth and Tax Relief Reconciliation Act of 2001(EGTRRA), and was made permanent under the Pension Protection Act of 2006 (PPA). The value of using the Saver's Credit to reduce taxes you would otherwise pay cannot be discounted, neither can the opportunity cost of not funding one's retirement nest egg if you don't take advantage of this credit.

If you are a low-to-moderate income taxpayer, you can take steps now to save two ways for the same amount. With the Saver’s Credit you can save for your retirement and save on your taxes.

|

|

|

Among those who are not saving for retirement, the Saver's Credit might just be the nudge that they need to start.

As usual, we turned to the IRS to find out what there is to know about the saver’s credit for the current year.

|

|

|

|

|

| First of all, eligible taxpayers still have time to make qualifying retirement contributions and get the Saver’s Credit on their 2017 tax return. You have until April 17, 2018, to set up a new individual retirement arrangement or add money to an existing IRA for 2017. |

|

However, elective deferrals (contributions) must be made by the end of the year to a 401(k) plan or similar workplace program, such as a 403(b) plan for employees of public schools and certain tax-exempt organizations, a governmental 457 plan for state or local government employees, or the Thrift Savings Plan for federal employees.

If you are unable to set aside money for this year, you may want to schedule your 2018 contributions soon so your employer can begin withholding them in January. |

|

| The saver’s credit can be claimed by any taxpayer who is: |

|

|

|

|

|

- Not a full-time student; and

|

|

- Not claimed as a dependent on another person’s return.

|

|

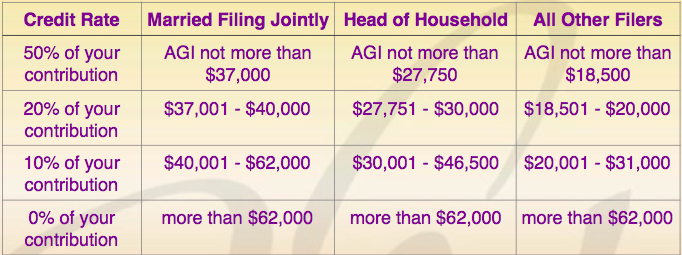

The amount of the credit is 50%, 20% or 10% of your retirement plan or IRA contributions of up to $2,000 ($4,000 if married filing jointly), depending on your adjusted gross income (reported on your Form 1040 or 1040A).

The maximum credit is $1,000 for single filers or individuals and $2,000 for married couples. |

|

| The credit amount is based on your filing status, adjusted gross income, tax liability and amount contributed to qualifying retirement programs. |

|

|

Here are the figures for 2017:

|

|

|

|

|

The saver’s credit is available in addition to any other tax savings that apply. Even better than the short-term tax benefits, this could mean quite a lot to you over the long run, during several years of retirement contributions.

Further, the maximum credit amount is the lesser of either $1,000 or the tax amount the eligible taxpayer would have had to pay without the credit. |

|

The Saver's Credit can be used to offset the individual's income-tax liability. In the determination of the Saver's Credit amount, refundable credits and the adoption credit are not taken into consideration.

|

|

Those who are eligible to receive the Saver's Credit are at risk of missing it if they use the wrong tax form. The Saver's Credit is not available on Form 1040EZ. If you are eligible to claim the Saver's Credit, you should use Form 1040, Form 1040A or Form 1040NR.

Form 8880, Credit for Qualified Retirement Savings Contributions, is used to claim the credit and its instructions have details on figuring the credit correctly. |

|

| The Saver’s Credit can be taken for your contributions to a traditional or Roth IRA; your 401(k), SIMPLE IRA, SARSEP, 403(b), 501(c)(18) or governmental 457(b) plan; and your voluntary after-tax employee contributions to your qualified retirement and 403(b) plans. |

|

Rollover contributions (money that you moved from another retirement plan or IRA) aren’t eligible for the Saver’s Credit.

Though Roth IRA contributions are not deductible, qualifying withdrawals, usually after retirement, are tax-free. Normally, contributions to 401(k) and similar workplace plans are not taxed until withdrawn. |

|

When figuring this credit, you generally must subtract the amount of distributions you have received from your retirement plans from the contributions you have made.

Distributions from the individual's retirement plans during what is called the "testing period," may reduce the allowable saver's credit amount or result in the individual being ineligible for the credit. |

|

|

|

|

The testing period is the two years preceding the year for which the credit is claimed, or January 1 to April 15 of the year following the year for which the credit is claimed.

For instance, if the saver's credit is claimed for 2018, distributions that occur during tax years 2016 and 2017, and from January 1 to April 17, 2018, could affect the individual's eligibility to claim the credit.

You should also consider help from a professional in any decision that may impact your taxes and your plans for retirement. |

|

|

|