|

|

The major tax reform approved by Congress and signed by the President on December 22, 2017, commonly referred to as the Tax Cuts and Jobs Act, or TCJA, or simply tax reform, has brought many changes both to individuals and businesses as of January 2018. The 2018 tax returns will be the first ones to show the true impact of the TCJA provisions on taxpayers pockets although, if the recent federal government shut down drags on much longer, delays in processing the returns and in receiving refunds are to be expected.

|

|

|

|

|

|

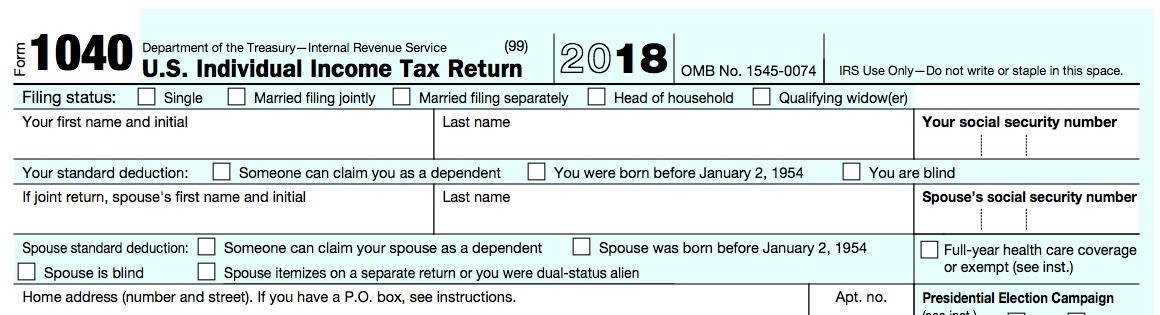

As a consequence of the tax reform, Form 1040 has been redesigned for 2018. The new design uses a "building block" approach.

The new Form 1040, which many taxpayers can file by itself, is supplemented with new Schedules 1 through 6. These additional schedules will be used as needed to complete more complex tax returns. The instructions for the new schedules are at the end of the Form 1040 instructions.

Forms 1040A and 1040-EZ are no longer available to file your 2018 taxes. If you used one of these forms in the past, you will now file Form 1040.

Some forms and publications that were released in 2017 or early 2018 (for example, Form W-2) may still have references to Form 1040A or Form 1040-EZ. Please disregard these references.

The deadline for filing Form 1040 for tax year 2018 is Monday, April 15, 2019. |

|

|

|

If you live in Maine or Massachusetts, you have until April 17, 2019, because of the Patriots’ Day holiday in those states and the Emancipation Day holiday in the District of Columbia.

Here is a summary of the most important changes that impact your taxes as of 2018.

For 2018, most tax rates have been reduced. The 2018 tax rates are 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

The standard deduction amount has been increased for all filers. The amounts are:

|

|

|

|

Single or Married filing separately--$12,000. |

|

|

|

|

Married filing jointly or Qualifying widow(er)--$24,000. |

|

|

|

|

Head of household—$18,000.

|

|

|

|

Personal exemption are suspended so you can no longer claim a personal exemption deduction for yourself, your spouse, or your dependents.

The maximum child tax credit has increased to $2,000 per qualifying child, of which $1,400 can be claimed for the additional child tax credit. In addition, the modified adjusted gross income threshold at which the credit begins to phase out has increased to $200,000 ($400,000 if married filing jointly). |

|

|

|

|

|

If you have a dependent, you may be able to claim the credit for other dependents. The credit is a nonrefundable credit of up to $500 for each eligible dependent who can't be claimed for the child tax credit. The child tax credit and credit for other dependents are both figured using the Child Tax Credit and Credit for Other Dependents Worksheet and reported on line 12a.

Beginning in 2018, you may be able to deduct up to 20% of your qualified business income from your qualified trade or business, plus 20% of your qualified real estate investment trusts dividends and qualified publicly traded partnership income. The deduction can be taken in addition to your standard deduction or itemized deductions.

For 2018, there have been important changes to the itemized deductions that can be claimed on Schedule A. These changes include:

|

|

|

|

Your overall itemized deductions are no longer limited because your adjusted gross income is over a certain limit.

|

|

|

|

|

Your deduction of state and local income, sales, and property taxes is limited to a combined, total deduction of $10,000 ($5,000 if married filing separately).

|

|

|

|

|

You can no longer deduct job-related expenses or other miscellaneous itemized deductions that were subject to the 2%-of-adjusted-gross-income floor.

|

|

|

|

|

|

|

|

The alternative minimum tax (AMT) exemption amount is increased to $70,300 ($109,400 if married filing jointly or qualifying widow(er); $54,700 if married filing separately). The income levels at which the AMT exemption begins to phase out have increased to $500,000 ($1,000,000 if married filing jointly or qualifying widow(er)).

On the new Form 1040 some lines have been combined or shifted to other forms and schedules. Some items that remain basically unchanged are:

|

|

|

|

the spaces for names and Social Security numbers, |

|

|

|

|

the spaces for signatures remain on page one, |

|

|

|

|

the checkboxes for selecting the Filing Status and

|

|

|

|

|

the checkboxes for the Presidential election campaign. |

|

|

|

The checkbox for reporting full year health care coverage or exemption is on page one of the 2018 Form 1040.

If your return is more complicated (for example you claim certain deductions or credits, or owe additional taxes) you will need to complete one or more of the new Form 1040 Schedules. Here is a general guide to what Schedule(s) you will need to file, based on your circumstances.

Schedule 1, Additional Income and Adjustments to Income, is needed if you have additional income, such as capital gains, unemployment compensation, prize or award money, gambling winnings. You can also use it if you have any deductions to claim, such as student loan interest deduction, self-employment tax, educator expenses.

Schedule 2, Tax, is used if you owe any alternative minimum tax or need to make an excess advance premium tax credit repayment.

Schedule 3, Non-refundable Credits, is for you to claim a nonrefundable credit other than the child tax credit or the credit for other dependents, such as the foreign tax credit, education credits, general business credit.

|

|

|

|

|

Schedule 4, Other Taxes, is needed if you owe other taxes, such as self-employment tax, household employment taxes, additional tax on IRAs or other qualified retirement plans and tax-favored accounts.

Schedule 5, Other Payments and Refundable Credits, is for taxpayers who can claim a refundable credit other than the earned income credit, American opportunity credit, or additional child tax credit.

You can also use Schedule 5 if you have other payments, such as an amount paid with a request for an extension to file or excess social security tax withheld.

Schedule 6, Foreign Address and Third-Party Designee, is necessary if you have a foreign address or a third party designee other than your paid preparer.

If you or someone in your family had health coverage in 2018, the provider of that coverage is required to send you a Form 1095-A, 1095-B, or 1095-C (with Part III completed), that lists individuals in your family who were enrolled in the coverage and shows their months of coverage. You may use this information to help complete Schedule 4, line 61.

You should receive the Form 1095-A, 1095-b, or 1095-C by early February 2019, if applicable. You don’t need to wait to receive your Form 1095-B or 1095-C to file your return. You may rely on other information about your coverage to complete Schedule 4, line 61. Do not include Form 1095-A, Form 1095-B, or Form 1095-C with your tax return. |

|

If you or someone in your family was an employee in 2018, the employer may be required to send you a Form 1095-C. Part II of Form 1095-C shows whether your employer offered you health insurance coverage and, if so, information about the offer. You should receive Form 1095-C by early February, 2019. This information may be relevant if you purchased health insurance coverage for 2018 through the Health Insurance Marketplace and wish to claim the premium tax credit on Schedule 5, line 70.

However, you do not need to wait to receive this form to file your return. You may rely on other information received from your employer. If you don’t wish to claim the premium tax credit for 2018, you don’t need the information in Part II of Form 1095-C. For more information on who is eligible for the premium tax credit, see the Instructions for Form 8962. |

|

|

|

|

Since the majority of taxpayers now use tax software, the IRS expects the change to this form and new schedules to be seamless for those who take advantage of the benefits of e-filing because the tax return preparation software will automatically use taxpayer answers to the tax questions to complete the 2018 Form 1040 and any needed numbered schedules.

Nevertheless, considering the numerous changes brought by the TCJA, we think that it is now even more necessary to use a tax professional in all your dealings with the IRS so you can have a safe and peaceful start to a prosperous 2019. |

|

|

|