|

|

Legalization of marijuana is a debatable subject, without a doubt. But, as you know, the main purpose of our newsletters has always been to offer you news and information on tax topics of general interest, without taking any stand. The subject of marijuana legalization makes no difference.

|

|

|

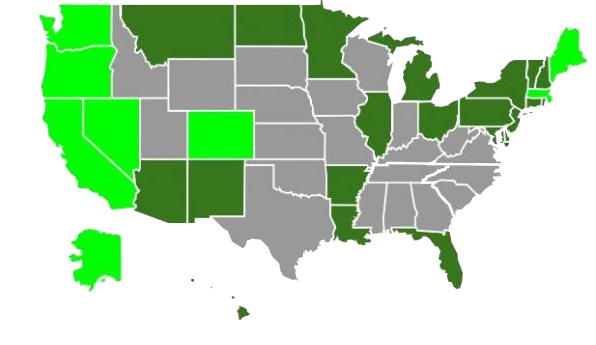

Fact check: at present, a number of 29 states and the District of Columbia are allowing some form of legal marijuana, and 8 have approved laws enabling the sale for recreational use.

|

|

|

|

The question is, what is the taxation at state and federal levels for the cannabis businesses?

Domestically grown marijuana is thought to be the second most profitable cash crop in the United States, only corn is considered to be more lucrative. To give you some pertinent figures, in 2015 alone, Colorado took in more than $135 million in tax revenue, which is more than double what it raised in 2014, and even surpassed the amount brought in by alcohol, too.

As it usually happens at state level, taxes can differ considerably, but for legal marijuana businesses they usually include state taxes, excises taxes, and wholesale taxes on both medical and retail cannabis. Medical marijuana is more loosely regulated and less taxed than recreational marijuana.

|

|

|

For instance, Colorado applies the following taxes: medical - 2.9% state tax, retail - 2.9% state tax plus 10% excise tax, and wholesale - 15% excise tax. Connecticut collects $3.50 per gram in medical tax, while Washington, DC is currently prohibited by federal law from taxing marijuana (DC has fully legalized recreational and medical marijuana, but recreational commercial sale is still blocked by Congress.)

While states have been rewriting their laws to legalize marijuana for either medical or recreational use, possession of marijuana remains a federal crime.

|

|

Under federal law, marijuana is still classed as a Schedule I drug which means that it is not legal in any form, including for medical purposes. It is, in fact, against federal law to grow, sell or use marijuana for any purpose.

|

|

| The Controlled Substances Act, passed in 1970, criminalized the possession or sale of marijuana. Possession of marijuana can result in felony charges in many states. A felony conviction can mean that you are not legally able to vote, own a gun, or enlist in the Armed Forces. As tax consequences, a felony conviction on a drug charge bars you from claiming the American Opportunity Tax Credit. You can also lose eligibility for financial aid. |

|

In the so-called Cole memo of 2013, the Department of Justice acknowledged the reality that most drug enforcement is carried out by state and local (not federal) authorities. The department's position has been that as long as state legalization efforts didn't threaten certain federal priorities — like keeping marijuana out of the hands of minors, preventing driving while under the influence of drugs and keeping marijuana grow operations out of federal lands — it would exercise “prosecutorial discretion” and direct its limited law enforcement resources to other drug priorities, such as dealing with the opiate epidemic.

This guidance that allows states to legalize marijuana without federal interference has remained in effect so far.

In any case, the IRS requires that taxpayers report all income from whatever source derived, (unless otherwise excepted) and that includes all illegal activities. |

|

| The IRS actually has a program, the Illegal Source Financial Crimes Program, that attempts to enforce taxation rules on income obtained through illegal operations which would otherwise be part of the untaxed underground economy. |

|

|

Taxation of cannabis trading is regulated by Section 280E of the Internal Revenue Code which forbids businesses from deducting ordinary business expenses from gross income associated with the trafficking of Schedule I or II substances, as defined by the Controlled Substances Act.

Section 280E was passed by Congress in 1982 in response to a case where the Tax Court ruled that a taxpayer could deduct expenses relating to his sales of cocaine, amphetamine, and marijuana. Deductible expenses included the costs of packaging, travel, and even scales used to weigh the illegal substances. |

|

|

| Section 280E states that, |

|

|

|

“No deduction or credit shall be allowed for any amount paid or incurred during the taxable year in carrying on any trade or business if such trade or business (or the activities which comprise such trade or business) consists of trafficking in controlled substances (within the meaning of schedule I and II of the Controlled Substances Act) which is prohibited by Federal law or the law of any State in which such trade or business is conducted.”

|

|

|

The IRS has subsequently applied Section 280E to state legal cannabis businesses, since cannabis is still a Schedule I substance.

|

|

In January 2015, the IRS issued an internal memorandum on how state-legal cannabis businesses should compute federal income taxes. The memo didn't reverse course on the deductions issue but suggested that a careful consideration as to the characterization of certain activities might result in legitimate reductions in tax.

What this means in fact is that ordinary and necessary business expenses, such as employee salaries, utilities, health insurance premiums, marketing and advertising costs, repairs and maintenance, rental fees, payments to contractors, which may roughly account for 40% of most businesses net income, cannot be applied to reduce the taxable income of cannabis businesses unless they can be allocated to Costs of Goods Sold (COGS). |

|

For marijuana growers, COGS includes expenses directly related to production of the plants, such as the seeds, electricity, and labor that went into growing and preparing the flowers for sale. Cannabis businesses have also followed guidance from section 263A of the IRC, which allows businesses to capitalize on indirect costs such as administrative and inventory costs, as well as the amount paid in state excise taxes and deduct them under COGS.

For marijuana dispensaries, COGS is much more restrictive, and generally includes only the amount they paid for the cannabis products they sell plus a few additional allocations.

The federal taxation of the cannabis industry is crucial in determining the state tax since most states tax calculations start with federal adjusted gross income (although certain states require adjustments to it). |

|

| Another particularity of the business is that, even in states that have legalized cannabis, banks are wary of doing business with companies that derive their revenue from the industry, for fear of coming into conflict with the federal drug law. Therefore, thousands of companies involved in the cannabis industry are compelled to conduct nearly all transactions in cash. As a result, such businesses are forced to keep a lot of cash on hand, making them susceptible to robberies, safety concerns (with special security expenses involved), and highly possible IRS audits. |

|

All these issues derived from discrepancies between states and federal regulations, as well as other specific difficulties, have determined lawyers, accountants, and other tax professionals to offer specialized services for this particular industry.

|

|

| If you are already in the cannabis business or just contemplating it, seeking help from professionals must be among your top priorities. |

|

|

|

|