|

|

All of you income earners everywhere are certainly (and sometimes painfully) aware that most types of income are subject to federal taxes and that income which is not subject to withholding taxes may be subject to estimated tax.

Whether the untaxed money comes from a job, investments, alimony or prizes, the IRS is demanding taxes owed, based on the well-known “pay-as-you-go” principle that the U.S. tax system is based on, which means that you must pay income tax as you earn or receive your income during the year.

|

|

|

|

|

|

According to the IRS, you don’t have to pay estimated tax for 2019 if you meet all three of the following conditions.

- You had no tax liability for 2018.

- You were a U.S. citizen or resident alien for the whole year.

- Your 2018 tax year covered a 12-month period.

|

|

|

|

You also don’t have to pay estimated taxes unless you have untaxed income, as estimated tax is the method used to pay tax on income that isn’t subject to withholding.

If the amount of income tax withheld from your salary or pension is not enough, or if you receive income such as interest, dividends, alimony, self-employment income, capital gains, prizes and awards, you may have to make estimated tax payments. If you are in business for yourself, you generally need to make estimated tax payments.

Estimated tax is used to pay both income tax and self-employment tax, as well as other taxes and amounts reported on your tax return.

If you receive salaries and wages, you may be able to avoid paying estimated tax by asking your employer to take more tax out of your earnings. To do this, file a new Form W-4, Employee Withholding Allowance Certificate, with your employer.

Those of you who receive Social Security benefits, unemployment compensation and certain other government payments can also choose to have federal tax taken out by filling out Form W-4V, Voluntary Withholding Request, and giving it to their payer.

|

|

|

|

|

To figure your estimated tax, you must figure your expected adjusted gross income, taxable income, taxes, deductions, and credits for the year.

In most cases, you must pay estimated tax for 2019 if both of the following apply:

1) You expect to owe at least $1,000 in tax for 2019, after subtracting your withholding and refundable credits.

2) You expect your withholding and refundable credits to be less than the smaller of:

|

|

|

|

90% of the tax to be shown on your 2019 tax return, or

|

|

|

|

|

100% of the tax shown on your 2018 tax return. (Your 2018 tax return must cover all 12 months.)

|

|

|

|

However, the 100 percent threshold is increased to 110 percent if your adjusted gross income is more than $150,000, or $75,000 if married and filing a separate return.

|

|

|

The percentages mentioned may be different if you are a farmer, fisherman, or higher income taxpayer.

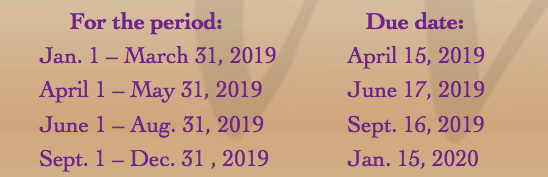

For estimated tax purposes, the year is divided into four payment periods. Each period has a specific payment due date. If you do not pay enough tax by the due date of each of the payment periods, you may be charged a penalty even if you are due a refund when you file your income tax return.

If a payment is mailed, the date of the U.S. postmark is considered the date of payment. Here are the payment periods and due dates for year 2019 estimated tax payments. |

|

|

|

|

|

|

|

|

|

You do not have to make the payment due on January 15, 2020, if you file your 2019 tax return by January 31, 2020 and pay the entire balance due with your return.

If you do not pay enough tax through withholding and estimated tax payments, you may be charged a penalty. You also may be charged a penalty if your estimated tax payments are late, even if you are due a refund when you file your tax return.

The penalty rate for the underpayment of estimated taxes may differ from year to year, and the amount of your penalty depends on your particular circumstances.

For 2018, a 5% rate applies for the following periods: April 16 through June 30, July 1 through September 30, and October 1 through December 31.

The IRS announced that interest rates will increase to 6% for the calendar quarter beginning January 1, 2019.

The rate for noncorporate tax payers is based on the federal short-term rate plus 3 percentage points. This rate is determined by the IRS on a quarterly basis.

If you think you owe the penalty, but you don’t want to figure it yourself when you file your tax return, you may not have to. Generally, the IRS will figure the penalty for you and send you a bill. |

|

The penalty for the underpayment of estimated taxes is figured separately for each payment period of estimated taxes. In order to figure your penalty amount, you must use Form 2210, Underpayment of Estimated Tax by Individuals, Estates, and Trusts, which contains both a short and a regular method for determining your penalty.

|

|

|

|

|

| Essentially, you must first determine the amount of tax that you have underpaid. Form 2210 can guide you through the process of figuring your penalty amount, which is directly based on the amount of your tax underpayment. |

|

|

Penalty Relief for 2018 Estimated Tax

|

|

On March 22, 2019, the IRS provided additional expanded penalty relief to taxpayers whose 2018 federal income tax withholding and estimated tax payments fell short of their total tax liability for the year.

The IRS is lowering to 80 percent the threshold required to qualify for this relief. Under the relief originally announced on Jan. 16, the threshold was 85 percent. As mentioned earlier, the usual percentage threshold is 90 percent to avoid a penalty.

This means that the IRS is now waiving the estimated tax penalty for any taxpayer who paid at least 80 percent of their total tax liability during the year through federal income tax withholding, quarterly estimated tax payments or a combination of the two.

The revised waiver computation will be integrated into commercially- available tax software and reflected in the forthcoming revision of the instructions for Form 2210.

Taxpayers who have already filed for tax year 2018 but qualify for this expanded relief may claim a refund by filing Form 843, Claim for Refund and Request for Abatement, and include the statement “80% Waiver of estimated tax penalty” on Line 7. This form cannot be filed electronically.

The expanded relief will help many taxpayers who owe tax when they file, including taxpayers who did not properly adjust their withholding and estimated tax payments to reflect an array of changes under the Tax Cuts and Jobs Act, the far-reaching tax reform law enacted in December 2017. |

|

|

|

|

It is also worth mentioning that exceptions to the penalty and special rules apply to some groups of taxpayers, such as farmers, fishers, casualty and disaster victims, those who recently became disabled, recent retirees, those who base their payments on last year’s tax and those who receive income unevenly during the year.

IRS Publication 505, Tax Withholding and Estimated Tax for use in 2019, is your complete resource on withholding and estimated payments.

As always, we recommend that you rely on professional advice to make sure you don’t underpay or overpay your taxes, estimated or otherwise. |

|

|

|