|

|

In the U.S. tax history, tax withholding is a relatively new concept, the system having been fully and permanently implemented only after the World War Two, and a few of today’s retiree may still remember a time without tax withholding.

|

|

|

|

|

|

|

|

The federal withholding system provides the model that 41 states use to withhold state income taxes. Nine states: Alaska, Florida, New Hampshire, Nevada, South Dakota, Tennessee, Texas, Washington and Wyoming don't have a state income tax.

|

|

|

The U.S. income tax is a pay-as-you-go tax, and there are two ways to pay as you go: withholding and estimated tax.

Under today's tax withholding system, taxes are collected at the source, meaning that wage earners never see the money that they owe in taxes, it’s taken out of their paychecks and transmitted directly to the federal government by their employers.

Independent contractors aren't subject to withholding, and neither is the income earned by investors, but individuals are responsible for calculating and remitting their own tax payments on a quarterly basis.

|

|

|

| The general rule for everybody is that at least 90% of taxes owed is either withheld on each paycheck or paid in estimated taxes throughout the year. |

|

|

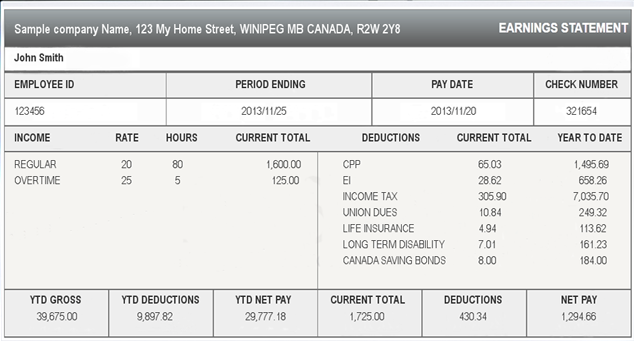

| Payroll withholdings include: |

|

|

|

Federal income tax; |

|

|

|

|

State income tax; |

|

|

|

|

Employee portion of Social Security tax; |

|

|

|

|

Employee portion of Medicare tax; |

|

|

|

|

Court-ordered withholdings; |

|

|

|

|

Other withholdings. |

|

|

| Federal Income Tax |

|

Employers are required to withhold the federal income tax that an employee is expected to owe based on salaries or wages.

The amount withheld for federal income tax is based on the employee's salary or wages as well as personal information that the employee is required to provide the employer on federal form W–4 (including marital status and the number of dependents claimed as exemptions). In cases where an employee is paid low wages and/or has a large number of personal exemptions, it may not be necessary for the employer to withhold any federal income tax. |

|

|

|

|

Each year the IRS publishes tables of the federal income tax rates. In 2017 the amount for one withholding allowance on an annual basis is $4,050 (same as 2016). Employers are supposed to start using the revised withholding tables and correct the amount of Social Security tax withheld at the beginning of the year, but not later than mid February.

Employers and payroll companies handle the withholding changes, so employees typically do not need to take any additional action, such as filling out a new W-4 withholding form. |

|

| It is important to know that you should check your withholding when any of the following situations occur: |

|

- You receive a paycheck stub (statement) covering a full pay period in the year, showing tax withheld based on annual tax rates.

|

|

- You prepare your previous year tax return and get a big refund, or a balance due that is:

|

|

|

| - |

More than you can comfortably pay, or |

|

|

| - |

Subject to a penalty. |

|

|

- There are changes in your life or financial situation that affect your tax liability.

|

|

- There are changes in the tax law that affect your tax liability.

|

|

| If you find you are having too much tax withheld because you did not claim all the withholding allowances to which you are entitled, you should give your employer a new Form W–4. Your employer cannot repay any of the tax previously withheld. |

|

However, if your employer has withheld more than the correct amount of tax for the Form W–4 you have in effect, you do not have to fill out a new Form W–4 to have your withholding lowered to the correct amount. Your employer can repay the amount that was incorrectly withheld. If you are not repaid, your Form W–2 will reflect the full amount actually withheld.

|

|

|

| If you claim exemption from withholding, your employer will not withhold federal income tax from your wages. The exemption applies only to income tax, not to Social Security or Medicare tax. |

|

|

State Income Tax

|

|

|

As mentioned above, the income state tax, for the 41 states that require it, works pretty much like the federal income tax; of course rates differ from state to state.

|

|

| The FICA Tax |

|

Federal Insurance Contribution Act (FICA) taxes, which include contributions to federal Social Security and Medicare programs, must be paid by all American workers, whether they are employed by a company or are self-employed.

The FICA tax is withheld from an employee's salary or wages and the employer is also required to pay a FICA tax. In other words, the employer is responsible for remitting to the federal government both the employee and the employer portions of the FICA tax.

Social Security accounts for 6.2% of the FICA tax, while Medicare accounts for 1.45%.

Employers are also required to match the 7.65% contributed by every employee, so that the total FICA contribution is 15.3%.

Self-employed persons are required to pay both the employer and employee portions of the FICA tax. |

|

|

|

|

For 2017, the new Social Security wage base is $127,200 — a substantial increase from the $118,500 level applicable in 2016. As a result of this increase, an employee making an amount equal to or greater than the Social Security wage base in 2017 could see his or her share of Social Security taxes increase to $7,886.40 — or $539.40 higher than the maximum payable in 2016.

Unlike Social Security, the amount of compensation subject to the 1.45% Medicare FICA tax is uncapped.

The additional Medicare tax of 0.9 percent for employees (not employers) remains in effect and must be withheld from employee wages that exceed $200,000 in a calendar year, at the beginning in the pay period in which the employee’s wages exceed $200,000. |

|

| Court-Ordered Withholdings |

|

| Courts of law may order employers to withhold money from an employee's salary or wages for purposes such as paying child support or repaying debts. |

|

| Other withholdings are voluntary and include: |

|

|

|

union dues; |

|

|

|

|

charitable contributions; |

|

|

|

|

insurance premiums; |

|

|

|

|

401(k) and 403(b) contributions; |

|

|

|

|

U.S. savings bonds purchases; |

|

|

|

|

payments owed to the company for the purchase of company merchandise. |

|

|

|

A Net Investment Income Tax went into effect in 2013. The 3.8 percent Net Investment Income Tax applies to individuals, estates and trusts that have certain investment income above certain threshold amounts.

Tax withheld from a foreign worker is referred to as non-resident alien, or NRA, withholding, and is different from regular income tax withholding. |

|

|

|

|

Unlike resident aliens and U.S. citizens who are taxed on worldwide income, non-resident aliens are subject to taxation on income from U.S. work. The typical withholding percentage is 30%, although exemptions are allowed, which can lower this percentage.

You can find all the information on the subject in Publication 505 (2017), Tax Withholding and Estimated Tax, on the IRS website. |

|

|

|

|

|

|

|

|